Fraud is an unlawful crime in which an actor intentionally deceives a victim in order to gain something of monetary value. It is a deliberate act of deceit, misrepresentation, or manipulation that can cause significant harm to individuals and businesses. The amount of money lost to fraud each year is staggering with over $8.8 billion in the United States alone in 2022.

Fraud is a growing problem that can have a devastating impact on individuals and businesses. With advancements in technology, fraud has been increasing in scale, complexity, and diversity across multiple industries and sectors. The prosperity of the Internet has also contributed to expanding the reach of fraudsters, while social engineering techniques have become increasingly prevalent and steal personal information by manipulating human psychology.

What are the different types of fraud?

Fraud can take various forms and target different individuals. Some of the most popular fraud types that have gained prominence in recent years include:

- Identity Theft: This involves stealing someone's personal information, such as name, social security number, or financial account details to carry out fraudulent activities.

- Online Purchase Scams: These scams occur on e-commerce platforms, where fraudsters advertise and sell counterfeit products, collect payment without delivering the goods or use stolen credit card information to make fraudulent purchases.

- Business Email Compromise (BEC): BEC scams involve impersonating company executives or employees to trick individuals within organizations into transferring funds or revealing sensitive information. These scams often target individuals responsible for wire transfers.

- Ponzi Schemes: Fraudulent investment schemes promise high returns to investors but instead use funds from new investors to pay off earlier investors. Ponzi schemes collapse when there are no new investors, causing substantial financial losses.

- Credit Card Fraud: Credit card fraud encompasses various activities, such as stolen card information, unauthorized charges, or counterfeit card creation. Fraudsters obtain credit card details and use them for unauthorized transactions.

- Insurance Fraud: This type of fraud involves individuals submitting false insurance claims, exaggerating losses, or staging events to receive undeserved insurance payouts.

In addition to the frauds described above there are many other forms of fraud including healthcare fraud, tax fraud, online dating scams, and phishing scams. Fraudsters continuously invent and adopt new tactics, and emerge new types of fraud over time. Awareness, vigilance, and education are key in protecting yourself and mitigating the risk of falling victim to fraud.

Fraud Detection Methods

Fraud detection methods encompass a range of techniques and approaches aimed at identifying and preventing fraudulent activities. Here are some commonly used fraud detection methods:

- Rule-Based Detection: Rule-based systems utilize predefined rules and patterns to flag potentially fraudulent activities. These rules are based on known indicators of fraud, such as transaction amounts, frequency, or specific behavioral patterns. When a transaction meets certain rule criteria, a transaction is flagged as potential fraud and triggers an alert for further investigation.

- Anomaly Detection: Anomaly detection focuses on identifying deviations from normal patterns of behavior. Statistical models and machine learning algorithms are used to analyze data and detect unusual activities that may indicate potential fraud. This method is effective in detecting previously unknown or emerging fraud patterns.

- AI and Machine Learning: AI and Machine learning algorithms are employed to develop predictive models that can automatically detect fraudulent patterns. These models learn from historical data and adapt over time to identify new fraud patterns or adapt to evolving tactics used by fraudsters.

- Behavioral Analytics: Behavioral analytics utilizes data on user behavior, such as browsing patterns, transaction history, or login activities, to establish a baseline of normal behavior. Deviations from this baseline are flagged as potential fraud. This method is particularly effective in detecting fraud involving account takeovers or identity theft.

- Big Data Analytics: Big data analytics leverages advanced analytical techniques to process and analyze large volumes of data from various sources, including transaction records, social media, or sensor data. By uncovering patterns, correlations, and anomalies, big data analytics enhances fraud detection accuracy and enables the identification of sophisticated fraud schemes.

- Manual Detection: Fraud detection can also involve user knowledge and human investigation. Experienced fraud analysts apply their domain expertise to detect fraud indicators, conduct in-depth investigations, and make informed decisions based on their findings.

It's worth noting that combining multiple detection methods and employing a layered approach provides stronger fraud detection capabilities. Organizations often employ a combination of automated detection systems, data analysis, and human intervention to effectively detect and combat fraud. There are fraud detection tools available to combat frauds.

Conclusion

To effectively detect and mitigate fraud, individuals, and organizations can employ a range of strategies. Implementing robust fraud detection systems that utilize rule-based approaches, anomaly detection, machine learning, and big data analytics can help identify patterns, anomalies, and suspicious activities indicative of potential fraud.

Vigilance, proactive measures, and a layered defense strategy are essential in safeguarding against the ever-evolving tactics employed by fraudsters. By implementing these strategies, businesses can protect their financial interests, reputation, and customer trust, while individuals can safeguard their financial security and personal information.

Share this post

Author

Read the latest articles from Scott Seong

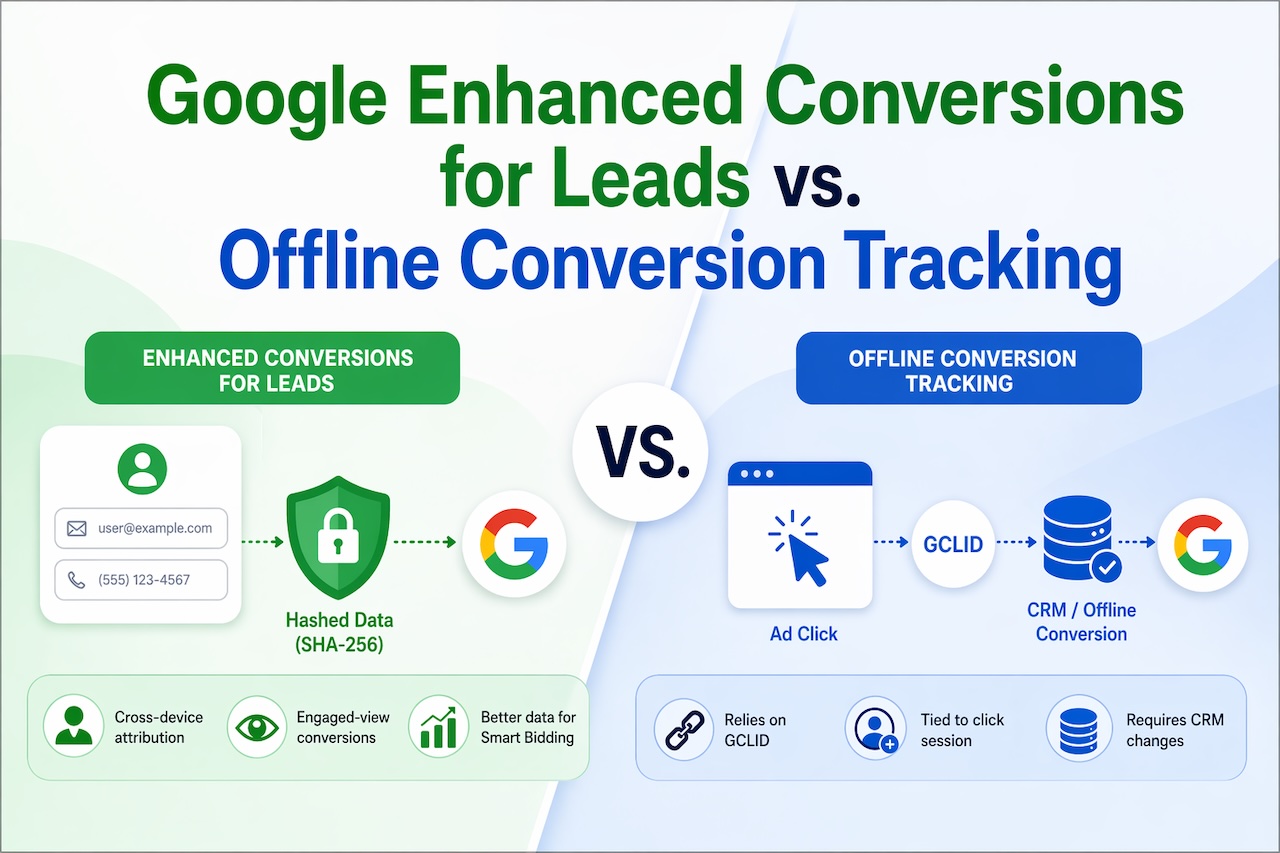

What are the differences between Google Enhanced Conversions for Leads vs. Offline Conversion Tracking?

April 24, 2026

These two features solve the same fundamental problem — lead gen advertisers can't see what happens after someone fills out a form — but they use different mechanisms to do it. Think of Offline Conversion Tracking (OCT) as the original solution, and Enhanced Conversions for Leads (EC4L) as its upgraded replac [...]

Learn moreAffiliate Marketing Explained: How to Turn Traffic into Revenue

April 15, 2026

Most people think making money online requires building a product, running ads, or managing a full business. But there’s another path that’s far more accessible—and often overlooked. Affiliate programs allow you to earn by simply connecting people with products or services they’re already interested in. Learn more

Leave a comment

All comments are moderated. Spammy and bot submitted comments are deleted. Please submit the comments that are helpful to others, and we'll approve your comments. A comment that includes outbound link will only be approved if the content is relevant to the topic, and has some value to our readers.

Comments (0)

No comment